What’s a SPAC? A simple guide to the investment trend.

What’s a SPAC? A simple guide to the investment trend.

You’ve probably heard or seen the acronym “SPAC” floating around in the last couple of months. It’s a craze that’s taken Wall Street by storm.

SPACs are special purpose acquisition companies, essentially shell companies that raise money from investors through stock-market listings. After going public themselves, they look for private companies to buy. Such transactions make those private companies public without having to go through the traditional initial public stock offering process, which involves “roadshows” to drum up investor interest and an intense media spotlight.

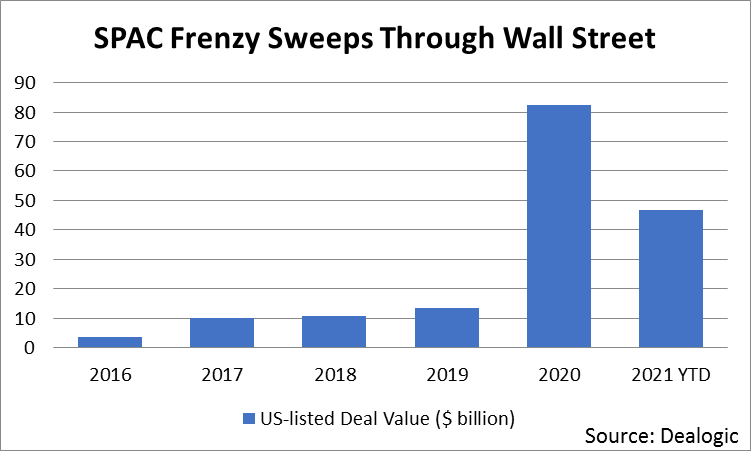

The total value of SPAC deals completed between 2019 and 2020 jumped 400%, according to data from Dealogic. And so far this year, the number of completed deals already totals more than half of those done in 2020.

Now bankers say the blockbuster trend is making its way across the Atlantic.

Just this week, the former boss of UniCredit, one of Italy’s biggest banks, teamed up with the founder of Louis Vuitton handbag maker LVMH to launch a SPAC aimed at buying a European financial company. And Klaus Hommels, an early investor in Spotify, launched his own tech-focused SPAC in Frankfurt, Germany’s financial center.

So, how do these investment vehicles work, and why have they become so popular?

Aloke Gupte, a top JPMorgan banker, organizes these kinds of deals in Europe, the Middle East and Africa, working with Morgan’s equity capital markets team. He broke down the process with the BBC’s Victoria Craig on the global edition of “Marketplace Morning Report.” Below is an edited transcript of their conversation.

Aloke Gupte: A SPAC is a special purpose acquisition company. And what that essentially is, is the vehicle which is listed on a particular exchange — could be in the U.S., could be in Europe. And that vehicle’s objective is essentially, in a fixed amount of time, to consummate an acquisition of a private company causing that private company to effectively become a listed company in its own right.

Choosing a SPAC over an IPO

Victoria Craig: It’s become a much more popular way of effectively going public. It’s just one of many ways. The way that we’re sort of all used to hearing about companies going public is the traditional initial public offering process, which involves a roadshow, lots of media attention, maybe a trip to the floor of the stock exchange where a company starts trading. Why would companies choose to forgo that process and do a SPAC deal over an IPO?

Gupte: Look, I think you hit the nail on the head. It’s a great question. It could do with a couple of things. One is with the nature of the business that the, the company has in the first place. So, for example, a company that is extremely well established, has huge revenues, is profitable, is a very well-known brand either in the broad market or in its own industry, is likely to always choose the IPO route. But a company which is slightly more early-stage, slightly more in a place where the proof of concept is not completely there or is in a sector which is a bit complicated for the layman or laywoman to understand, and where you can actually benefit by having a SPAC because a SPAC, crucially, allows a company to share with investors its forward business plan.

Particularly, when you look at, you know, auto-tech companies or electric-vehicle manufacturers, there are many of them. All of us know that there will be more electric vehicles on the street in 2030 than there are today. That is undoubtedly true. But the question is, whose vehicles will they be? We certainly know they’ll be Teslas, but what else? And in that light, I think these companies are able to use the SPAC route to better explain what they plan to do. You know, “I’m going to make an electric van, and this is how I’m going to do it. And this is my plan to be able to sell X number of vans by 2024,” thereby allowing investors to get a better and deeper understanding of what the company is seeking to do over a period of time, and value it better, and understand it better. You’ve also seen companies that might otherwise IPO choose the SPAC route. This is also because sometimes the SPAC route can be quicker.

The risk for SPAC investors

Craig: So from an investor perspective you know, sort of, the road map, the kinds of companies that these SPACs are looking to buy. But you don’t know the company specifically, do you? Is that a risk from an investor point of view?

Gupte: Yeah. Look, you certainly don’t know the company specifically. And that is very important from a disclosure perspective. I think what investors therefore look at is really what is the quality of the sponsor team? What kind of track record do they have? Whether it be an entrepreneurial track record, whether it be, you know, a vast amount of experience in the financial field, whether some of the sponsors, or all of the sponsors, have led publicly listed companies before. So they will look at all of those things and say, “Look, this sponsor team is a high-quality team. We don’t know what they’re going to acquire.” There’s probably a little bit of articulation around the sectors that they might look at. But, really, investors are looking at those individuals or those firms or sponsors who are setting up the SPAC and saying, “We believe these people will be able to execute a successful strategy. And on that basis, we will back them.”

Craig: And what happens if they don’t? What happens if that SPAC can’t find a company to acquire or if the deal falls apart? What happens then?

Gupte: That’s the beauty of the construct. The SPAC essentially has a 24-month period to get that acquisition. But if it does not in 24 months, investors’ capital is redeemed. This was a feature which basically led to the spurt in growth of SPACs in the U.S. because, essentially, investors are capital-protected. And you can now employ those structures in various locations in Europe as well.

What regulatory scrutiny do SPACs undergo?

Craig: Now, we sort of hit on the traditional IPO process. Without some of those bright lights and the scrutiny that we see, do these SPAC deals undergo the same kinds of regulatory scrutiny or investor scrutiny that the traditional IPO process involves?

Gupte: Yeah. Look, I mean, there is clearly a good degree of scrutiny because two things happen. When you actually do the acquisition, you do need to go to the market and raise funds at that point in time. You go to investors, a select group of investors, and say, “Look, the SPAC is planning to buy company X at a valuation of ABC. And would you investors, once you understand the business model and the business plan, would you sign up and be part of this exercise and help us raise more cash?”

So in that sense, the investor scrutiny or the validation of value, if you will, is submitted to at that point in time. It can’t simply be that the SPAC says, “I will buy you for X” and the company is happy, but that needs to get validated by the market.

Equally, from a regulator standpoint, there is a merger document that needs to be put together that becomes public. It’s hard to say whether the regulatory framework around this and the investor and market framework around it will evolve or not. I think it will. SPACs are still relatively young, so we will see continued evolution. But there certainly is a degree of scrutiny and focus in terms of how these transactions are put together.

SPAC growth in the U.S.

Craig: There’s been huge growth and demand for these vehicles, particularly in the U.S. Are there enough target companies for these SPACs to buy? Do you worry about the quality of the kinds of companies that are sort of in the crosshairs now?

Gupte: Look, I think it’s a great question. I think we are certainly right now in a market, in a world where there are a lot of private companies that are incredibly exciting because, you know, there is a digitalization happening across so many sectors. Now there’s auto tech, and there’s health tech. That said, we’ve got to also admit that there are more than 350 SPACs in the U.S. today. Clearly, I think, given the limited time frame that SPACs have, which is 24 months in which to consummate the acquisition, I would, if I had to hazard a guess, say something like maybe 20% or 25% of the SPACs don’t complete an acquisition. Maybe a few will do acquisitions which will be less than stellar. And, you know, hopefully, others will learn from those sorts of examples and not repeat those mistakes. I think a majority of them are really actually led by extremely strong sponsors who have great experience and deal-making chops. And I think that is going to result in them making good decisions in terms of the companies they acquire.

SPACs beyond U.S. borders

Craig: Do you think this is a trend? Like I said, this is a booming one in the U.S. Is this one you think will expand to other parts of the world?

Gupte: Undoubtedly, it will. And I think we are having this conversation on an appropriate day with one having been announced yesterday, which is listing in Amsterdam, and one transaction that we are running at this very moment, which is listing in Frankfurt.

There is a huge number of European as well as Asia-Pacific companies that would want to be listed, but would want to be listed in their own regions. And I think for those companies, it will be important that there is a local SPAC offering as well. And if you think about the parameters that sort of dictate whether a SPAC can successfully list or not, there are only a couple. One is, is it a SPAC structure which is sensible from an investor standpoint, i.e., the point I made earlier about them being able to redeem if they want to redeem? That can be employed in Europe and can be employed quite widely in London, in Amsterdam, in Stockholm, in Paris and in Frankfurt.

The second element is, is there fundamentally a pool of capital that is deep enough? The answer to that is undoubtedly yes. There is huge demand, not only from European investors, but from global investors. Now, where do those SPACs come up? You know, for example, the most natural listing home for a French company might be Paris. Similarly, for a German company, that might be Frankfurt, and for a U.K. company, that might be London. So that will be driven by the objectives of the teams that are looking to set up SPACs. I would expect to see them across all of the key listing locations in Europe. I think there is a lot of momentum behind this today.

Craig: Now with that German SPAC that you mentioned there, Lakestar, it seems like there was big demand for that. Is that sort of an indication of what we could see, what could be on the horizon for Europe, just a boom in demand just waiting to sort of explode?

Gupte: Absolutely. The demand pools are really, really deep. Hopefully there will be some exciting sponsors who will look to do SPACs in Europe to allow that demand to find its natural home.

Stories You Might Like

There’s a lot happening in the world. Through it all, Marketplace is here for you.

You rely on Marketplace to break down the world’s events and tell you how it affects you in a fact-based, approachable way. We rely on your financial support to keep making that possible.

Your donation today powers the independent journalism that you rely on. For just $5/month, you can help sustain Marketplace so we can keep reporting on the things that matter to you.