Haircut: More dangerous than it sounds

If Greece accepts the terms of a new aid package it’s expected to get a haircut on its debt. But Sr. Editor Paddy Hirsch explain why that haircut is more like a scalping — and it’s not Greece that will suffer the pain.

Such an innocuous word: haircut. It conjures up one of those Norman Rockwell images of a kid in a barber’s chair. Sometimes the kid is smiling, sometimes scowling. Either way, it’s just a haircut, no big deal. In a few weeks, the hair grows back and the kid comes back for another shearing. At some point in the cycle, everyone’s happy.

Not so if you’re a bank lending money to Greece, and you’ve agreed to a 50 percent haircut on that debt. This haircut is less like a trim at the local barber shop and more like a visit to “Sweeney Todd.” After this haircut, there’s no growing back. In this haircut, you’re agreeing to allow Greece to cut its debt to you in half. That’s a scalping.

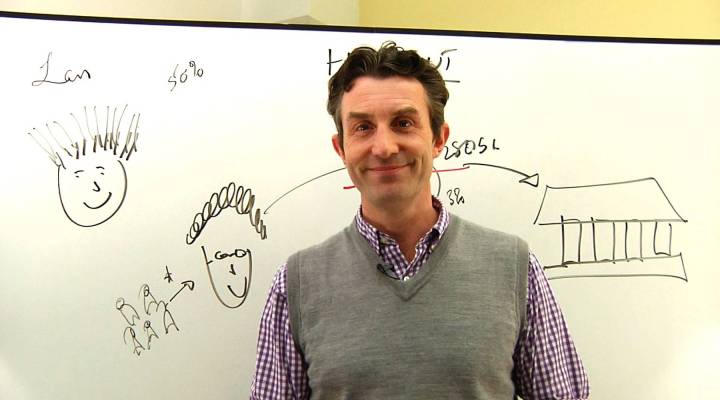

Greece owes about $280 billion to banks right now. That is, it has sold roughly $280 billion in bonds that the banks are holding. Under the bailout that the banks have agreed to, that debt will be cut in half: Greece will only owe the banks about $140 billion.

So Greece is happy(ish). But the banks are in a hole. Banks, of course, make their money from borrowing from depositors like you and I, and lending that money out… to countries like Greece. In other words, that $280 billion isn’t the banks’ money, it’s money that belongs to depositors. And those depositors are going to want that money back. And now, thanks to Greece, the banks are $140 billion short.

The question now is: Will the bank have the money it takes to pay its depositors? In the past, the thought that an institution might not have enough money to make its depositors good was enough to trigger a run on the bank. That would cause the bank to collapse. And because the world’s banks are tightly connected these days, one collapse can trigger the meltdown of the entire financial system.

That hasn’t happened yet in Europe; the banks have said they’ll be OK, and European governments say they’ll support the banks. But there are no guarantees. This is Europe, which is a coalition of sovereign governments, the individual leaders of which can throw a plan into disarray at any moment. Just look at Slovenia’s holdout on the plan, or Greek Prime Minister George Papandreou’s vacillation over a referendum on the bailout. This drama is still playing out, although it’s beginning to look more like Tarantino than Homer.

Stories You Might Like

There’s a lot happening in the world. Through it all, Marketplace is here for you.

You rely on Marketplace to break down the world’s events and tell you how it affects you in a fact-based, approachable way. We rely on your financial support to keep making that possible.

Your donation today powers the independent journalism that you rely on. For just $5/month, you can help sustain Marketplace so we can keep reporting on the things that matter to you.